How the UK water sector could further address whole-life carbon in its capital investments

The recent guidance from Ofwat on embodied carbon accounting is a welcome step in the right direction for the UK water sector. However, there isn’t a consistent time frame or end target date in place yet to achieve net zero across both investments and operations. Until whole-life carbon accounting is mandated and brought under a suitable regulatory framework, individual water companies may need to act independently to develop their own carbon reporting and management systems, say sustainability experts Ben Murray and Alex McMahon.

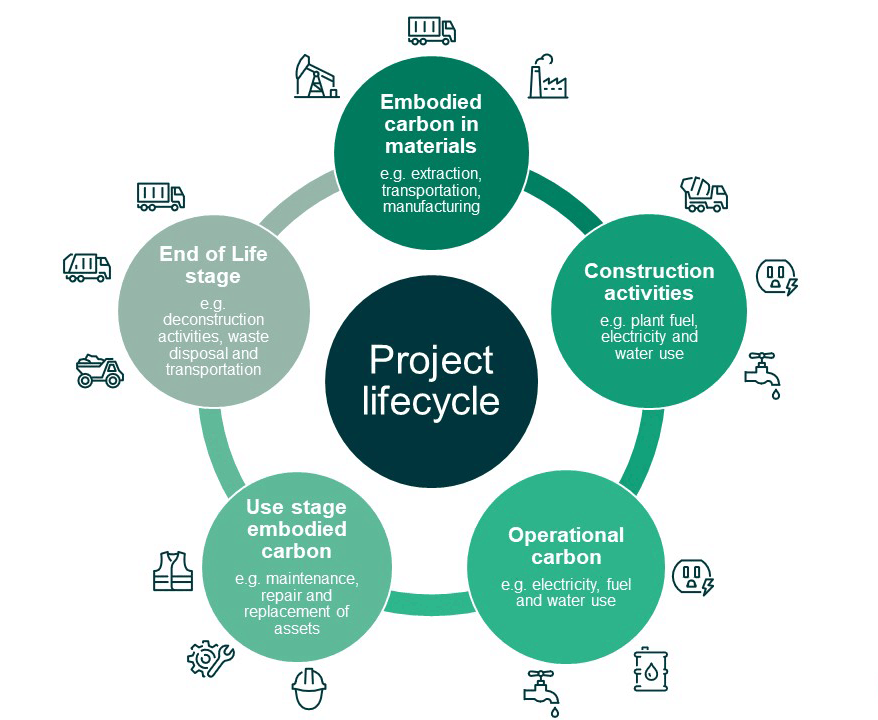

The water sector is a highly energy-intensive industry, and has a key role to play in helping the UK meet its legally-binding net-zero emissions targets. The focus to date has been almost entirely on monitoring and reporting operational carbon, and the UK water industry does this extremely well. However, the thorny problem of embodied carbon from capital expenditure still remains.

Ofwat recently published guidance regarding embodied carbon reporting, detailing ambitions for mandatory, standardised capital carbon reporting by 2022-23. But it needs to go further. Whole-life carbon management goes beyond the retrospective reporting of carbon emissions, and should embed carbon reduction into requirements and targets. Standardised monitoring and reporting is certainly important, but water companies still need toact as soon as possible to proactively design out the whole-life carbon resulting from their capital projects. A five-year wait for a sector-wide standardised approach is not on a par with other sectors’ net-zero ambitions.

This article discusses some ways the water sector’s approach to managing embodied carbon could be improved and developed, both at a shorter-term individual company level and a medium- to long-term sector level.

Embodied carbon accounting – current practice

English water companies have committed to achieve net-zero operational carbon emissions by 2030, with the water companies in Scotland, Wales and Northern Ireland working towards their own targets for emissions reduction.

For well over a decade, the UK water sector has used a standardised approach¹ for monitoring and reporting on its operational carbon emissions, using UK Water Industry Research’s Carbon Accounting Workbook (UKWIR CAW). However, there is no such common approach to accounting for or managing the embodied carbon emissions resulting from each company’s capital investment programme, nor are these emissions included in the Water UK net-zero target for 2030. While a number of UK water companies are now developing and using bespoke embodied carbon accounting tools, there is a long way to go to achieve the same level of standardisation across the industry that has been achieved for operational carbon.

Over time, embodied carbon may form an ever-greater share of overall emissions as operational emissions fall due to grid decarbonisation and an increase in self-generated renewables. This contribution is becoming increasingly recognised both by UK water companies and across the wider infrastructure sector, with more companies and organisations now explicitly including embodied carbon in their net-zero targets. The 2040 net-zero ambition that Scottish Water agreed with the Scottish Government in 2019 includes both operational and embodied emissions.

Ofwat guidelines

Despite UKWIR identifying a need to account for embodied carbon emissions almost a decade ago, Ofwat only recently highlighted this issue in their Regulatory Accounting Guidelines 2020-21 published in April 2021². While the embodied carbon accounting ambitions outlined in the guidance are commendable, the timescales suggested (i.e. mandatory, standardised embodied carbon reporting by 2022-23) are ambitious considering the work required to achieve sector-wide standardisation. Furthermore, the Ofwat guidance does not yet provide any detail around how this might be achieved, but Ofwat are planning to engage with key stakeholders later this year following on from the July Annual Performance Report submissions.

Ofwat’s ambition for mandatory, standardised embodied carbon reporting is a welcome step in the right direction. However, Ofwat will need to go further in future by explicitly identifying key projects in the current asset management plan period 2020-2025 that can be used as exemplar schemes, demonstrating how active carbon management can be integrated into planning, design and delivery to stimulate innovation, encouraging the use of lower-carbon materials, and maximising construction efficiency. At present however, the focus is solely on reporting and not on the tools needed to make sure carbon is factored into the decision-making process so that the infrastructure we build is fit for purpose in a low-carbon world.

Sector-wide steps (medium- and longer-term)

To reduce carbon emissions within the water sector most effectively, a standardised, sector-wide approach that includes both operational and embodied carbon emissions should be developed to improve understanding of embodied carbon impacts. Embodied carbon should also be included in carbon reduction targets. Here are some examples of best practice from other sectors and ways that whole-life carbon accounting and understanding could be improved.

1/Facilitate effective and standardised carbon accounting using sector-wide, whole-life carbon estimating tools

This is already being done in other UK sectors. For example, the Rail Safety and Standards Board has developed a Rail Carbon Tool which is used by Network Rail on all major projects across the sector.

Similarly, the Environment Agency has developed a suite of bespoke carbon estimator tools that can be used to produce high-level carbon assessments at optioneering stage, as well as more detailed assessments of the lifetime carbon impacts of projects when more detailed data is available. Our data experts are currently working with the Environment Agency to take this a step further still by developing a cutting-edge, integrated cost and carbon tool, which produces valuations for both cost and carbon from a single set of data.

2/Address the data gap

In terms of estimating embodied carbon, there are data sources available for many civil engineering-oriented materials and interventions commonly used within the water sector – for example, the typical carbon ‘big hitters’ such as concrete, steel, pipework and excavations. However, other items such as mechanical, electrical, instrumentation, control and automation (MEICA) and other fabricated components frequently lack any reliable emissions factors, and this data gap poses a real challenge.

To address existing gaps in the data, the sector should move away from industry-standard data to supplier-specific data. This could be achieved by including a requirement for carbon management, including the provision of reliable carbon data, to be incorporated into the procurement of all frameworks and contracts, and by embedding a standardised and reliable approach to reporting and managing carbon across the water sector’s common supply chain.

3/Make Environmental Product Declarations (EPD) a requirement

Where supplier-specific embodied carbon data is available, it is of limited use in decision making because it is not always verified by an independent third party. In the medium-term, this data quality could be improved further through independently verified Environmental Product Declarations (EPDs).

A timescale should be set to make EPDs a requirement (e.g. the start of AMP8, SR27 or other equivalents specific to devolved administrations or regional suppliers). This timescale should be agreed across the water sector and mandated by regulatory bodies such as Ofwat and the Water Industry Commission for Scotland (WICS).

Shorter-term steps for individual water companies to take

Until the above actions are taken, water companies should ideally assess the whole-life carbon impact of projects as early as possible in the planning and design process to allow proactive carbon reduction interventions to be identified and implemented.

1/Encourage the supply chain to provide reliable and transparent data on the carbon impact of the goods and services they provide.

2/Include carbon as a metric in the procurement process to drive innovation and carbon reduction within the supply chain.

3/Utilise third-party tools such as our ScopeX™ process that reduces carbon through design, across the entire project life cycle. The approach considers materials, site locations, logistics and construction methods to reduce and eliminate the impact of projects on the natural environment.

To remain aligned with other utilities and infrastructure providers, the sector needs to identify and implement proactive whole-life carbon management interventions on capital investment programmes. Until a standardised approach is agreed however, the onus is on either individual water companies – or groups of companies perhaps along those used for regional water resource resilience planning – to take the initiative. It is already happening elsewhere, and the water sector can use best practice from other sectors to accelerate the journey to net zero across both operations and capital investments.

¹ Operational carbon includes the industry’s scope 1 and 2 emissions, and some scope 3 emissions. Embodied carbon is overwhelmingly in scope 3

² Ofwat (April 2021), Information notice: Regulatory accounting guidelines 2020-21: Further guidance on reporting of greenhouse gas emissions